Achieving your financial goals doesn’t happen overnight; it takes careful planning and execution.

Financial planning is important as the process enables you to clearly identify your priorities and focus your resources on achieving your objectives.

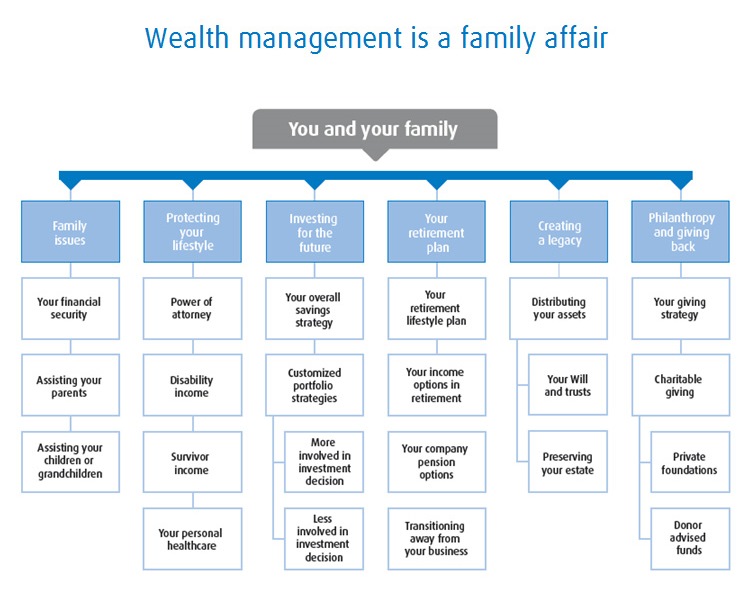

Why do you need a financial plan?

A good financial plan can help you answer these questions, and more...

- Will you be in a position to fund your children’s post-secondary education?

- Will you be responsible for the care of an aging parent or spouse, or a mentally or physically challenged child?

- Is your investment strategy consistent with your financial goals?

- If you were to die, would your family be financially secure?

- If you become disabled, will you have enough income to manage until you are well again?

Your Financial Plan

A financial plan provides you with a comprehensive assessment of your financial situation and helps you determine if your existing investment strategy is in line with your goals. Your plan includes a review of your:

Current financial position: Your financial position is a combination of your net worth (assets, minus liabilities) and your annual cash flow (income, less expenses and savings). This information provides an overview of the financial resources currently available to meet your goals.

Investment planning: A successful investment strategy begins with asset allocation. A review of the asset mix for each of your investments, registered and locked-in accounts is completed and then compared to what is being recommended for accounts with investment objectives similar to yours.

Education planning: By analyzing the expected costs and setting up a savings strategy, you can help ensure that your children get the education hey deserve.

Major purchase planning: If you have a major purchase on the horizon, such as a dream vacation, new vehicle or a vacation property, your existing savings strategy is compared to the future purchase cost to determine whether your current strategy will allow you to meet your goal.

Retirement planning: Combined sources of retirement income are measured against retirement goals to ensure you can maintain your desired lifestyle throughout retirement.

Estate planning: A summary of your estate’s distributable assets and obligations is provided (e.g., income taxes, probate costs and debts), including an overview of the income needs of the surviving spouse and if more capital is needed to support the survivor’s lifestyle.