Owning the Backbone of Change

Christine Fortin - May 25, 2026

Reflections from a Fireside Chat with CEO of Brookfield Infrastructure, Bruce Flatt

I had the unique opportunity in February of this year to be part of a fireside chat with Bruce Flatt. A rare visit to Canada on his way through from London UK to the Superbowl, with a stop in Toronto for the fireside (and, I’m sure some investment discussions and maybe even a visit with his old employee, Mark Carney).

There are moments in investing where the signal becomes unmistakable—when structural change moves from theory to inevitability.

My recent conversation with Bruce Flatt was one of those moments.

What emerged was not simply a set of trends, but a clearer view of what will matter most over the coming decades — and where capital must be deliberately positioned. Now, our clients know that we are one of the early adopters into infrastructure – adding it into the portfolio well over a decade ago. So, learning how this investment remains relevant in a changing economy for me personally was equal parts fascinating and confirming of our institutional led investment approach.

The Discipline of Compounding

At the centre of the discussion was a simple idea:

If you can compound capital at 12–14% over long periods of time, extraordinary outcomes follow.

Not through prediction.

Not through activity.

But through ownership — of the right assets, held long enough.

This perspective is crucial as we enter an unprecedented infrastructure build cycle. (I wrote this before the Carney announcement stating exactly this).

Recognizing Change—But Not Chasing It

A key lesson:

You do not need to be early. You need to be right.

The discipline is in waiting until a shift becomes real, essential, and economically viable — and then deploying capital with conviction.

We saw this in solar. What once required subsidies is now the lowest-cost form of power globally.

We are now seeing similar inflection points elsewhere — most notably in energy itself.

Don’t chase an asset until it becomes a solid investable choice. Meaning it is well integrated into daily society, until then, it is simply roulette – think bitcoin. Is the infrastructure there for bitcoin to support the long-term viability and implementation in daily commerce? Not yet. Thus, how can you make a confident investment without knowing the definitive revenue stream?

A More Consequential Observation: Energy Has Been Quietly Stable

For nearly 25 years, something unusual occurred:

Global energy consumption remained remarkably flat. FLAT. Think about what your home or office looked like 25 years ago and imagine that energy consumption hasn’t moved in 25 years.

Not because demand was stagnant — but because efficiency gains offset growth.

We used more devices, more computing power, more electricity —

but we also became better at using less.

That equilibrium is now breaking. We are expected to double energy consumption in the next 15 years. How is that even possible to build out the infrastructure to meet the demand?

Digitalization Is Now an Energy Story – spoiler alert: not which chip company to buy

The digital economy is often misunderstood as “light”.

In reality, it is becoming one of the largest drivers of electricity demand globally.

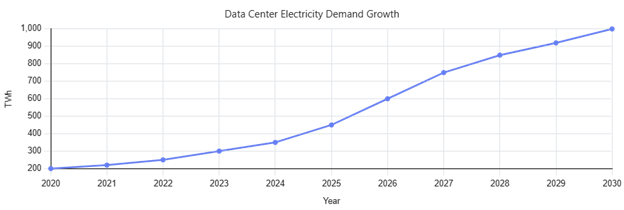

Data Centre Power Demand Growth

The Repricing of Power

We are entering a fundamentally different phase.

- Energy demand is now expected to increase dramatically over the next 10–15 years

- In many forecasts, electricity demand alone could double — driven by data centres, electrification, and industrial reshoring [newswire.ca], [thedeepdive.ca]

This is not incremental.

It is a structural break.

And importantly, it is not demand that is uncertain — it is supply.

As Bruce Flatt noted, the constraint is no longer technology.

The limiting factor is power — access to it, transmission of it, and the ability to build it at scale.

Digitalization Is Driving Physical Demand

One of the more misunderstood dynamics today is that the digital economy is becoming increasingly energy-intensive.

- Data centre electricity demand alone is expected to more than double by 2030 [gartner.com], [spglobal.com]

- AI infrastructure is rapidly becoming one of the largest incremental drivers of global electricity consumption

What appears intangible is, in reality, deeply physical.

Every layer of AI and cloud computing relies on:

- Power generation

- Grid connectivity

- Cooling and storage infrastructure

Which leads to a simple, but important conclusion:

The future of technology is constrained by the availability of energy.

How Are We Responding? A Canadian Case Study

What was particularly notable is that this shift is no longer just an investment theme — it is now public policy.

Today as I write, Thursday May 14th, Prime Minister Mark Carney announced Canada’s National Electricity Strategy — a direct response to these pressures. This is after building a Sovereign fund a couple of weeks ago, to encourage companies to partner in building out infrastructure. The announcements on resource partnerships and rebooting aging mines with rare minerals is happening at a pace not seen in my lifetime.

At its core:

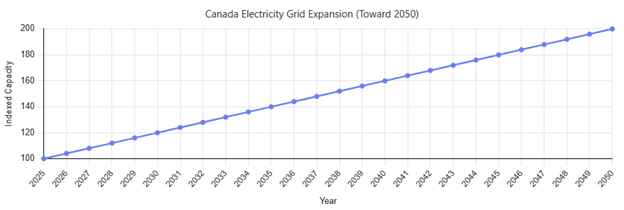

- Canada aims to double its electricity generation and grid capacity by 2050 [cbc.ca], [bloomberg.com]

- This will require over $1 trillion in investment, spanning generation, transmission, and storage [bloomberg.com]

- The plan includes:

- Expanding hydro, renewables, and nuclear

- Integrating provincial grids into a more unified national system

- Allowing natural gas to play a complementary role for reliability and baseload power [newswire.ca], [cbc.ca]

Importantly, this is not framed as optional.

It is framed as foundational.

Electrification underpins competitiveness, affordability, and energy security.

This aligns directly with what we heard from Brookfield:

The world is not just decarbonizing — it is rebuilding its entire energy system at scale.

The Scale of What Lies Ahead

The implication is difficult to overstate.

We are moving into a period where:

- Entire power grids must be rebuilt or expanded

- New asset classes (storage, transmission, distributed energy) become essential

- Capital requirements move from billions to trillions

Even within a single segment—data infrastructure—the scale has shifted dramatically:

- Projects once measured in hundreds of millions

- Now measured in tens of billions

This is not a typical investment cycle.

It is generational.

Why This Matters for Long-Term Capital

For families who think in decades, not quarters, this introduces a clear set of considerations:

1. Power Becomes the Defining Asset

Access to reliable energy will underpin:

- Economic growth

- Technological advancement

- Industrial competitiveness

2. Infrastructure Is No Longer Peripheral

It is central. The assets that generate, store, and move energy are becoming the backbone of the global economy.

3. Private Markets Will Play a Critical Role

Much of this buildout:

- Requires long-duration capital

- Demands operational expertise

- Exists beyond the reach of traditional public markets

- Governments simply don’t have the capital. The end.

- This is not an investment in your grandparent’s infrastructure (power plants etc.), this is an investment in your grandchildren’s infrastructure that will be sustainable and more efficient sources of power than current power generation.

4. Scarcity Drives Return. How to Capitalize on this concept (i.e.. what to Invest In)

The challenge is not identifying demand.

It is meeting it.

And that gap — between demand and deliverable supply — is where disciplined capital compounds.

This means that it will not be limited to building more power plants like we see today.

It means visiting alternatives:

- Nuclear

- Solar

- LNG

- WTE (waste to energy)

From our Grandparent’s Infrastructure to our Grandchildren’s Infrastructure: an Example of Accessing Power Generation of Today

Most will be handled through private markets. Specifically industrializing families who are pivoting and looking for boots on the ground investments. Note – Canada is an infrastructure superpower, and it is shocking how little we have. When Carney was in Davos, he only took 3 meetings and one of them was with an infrastructure private investment firm, EQT. The purpose was to solicit private investment to access our superpower buildout. (another was with a power wall plate company).

Private Market investments is currently 150 trillion for institutional and 150 trillion from private wealth. Specifically:

- Sovereign funds 24%

- Pension plans 17%

- Endowments 34%

- Insurance companies 7%

- Families (private wealth and family offices) 18%

** source: Hamilton Lane presentation at national alternative investment conference

Consider WTE (waste to energy). A company like ReWorld.

ReWorld is a municipal solid to waste to power company. In short, it burns trash and creates power.

- Converts non-recyclable waste into electricity and steam using high temperature processes.

- Produces continuous, baseload electricity – power is available 24/7 regardless of weather.

- It is cleaner than power plants

- It solves multiple issues including management of household waste.

- They source high margin trash (they pay for trash) so helps municipalities manage costs with respect to waste. The cost is less than municipalities paying to dump trash to landfills.

- They have long term contracts to ensure they have access to cash and then make money selling power.

- Most renewable energy sources are intermittent (wind, solar). This is 24/7.

- Growth of WTE is structurally growing driven by: urbanization, landfill restrictions, ESG mandates.

- Expanded from 50 – 90 facilities across North American (source waste dive)

- Have created integrated verticals:

- Alternative fuels (ReKiln)

- Wastewater treatment (ReDrop)

- Logistics (ReMove)

- Carbon offsets (ReCredit)

- Clean energy and circular economy business. Circular economy businesses *is* investing in our grandchildren’s economy and infrastructure.

This is an example of how we need to think differently about infrastructure investment and look for those opportunities which are available to accredited investors and hopefully will be mainstream for the masses at some point.

A Final Reflection

Perhaps the most telling point Bruce made was this:

Roughly half of what they own today did not exist as an investable asset class 15 years ago.

It is a quiet reminder.

The next decade of wealth creation will not come from familiar categories — but from owning the infrastructure that enables the next phase of global growth.

And increasingly, that comes back to one thing:

Power of the Future.

Not as a theme.

Not as a trade.

But as a foundational asset — essential, scarce, and deeply tied to how the world evolves from here.

References:

- Prime Minister Carney announces forthcoming National Electricity Strategy

- Canada Unveils C$1 Trillion Plan to Double Electricity Grid Capacity by 2050 | the deep dive

- Gartner Says Electricity Demand for Data Centers to Grow 16% in 2025 and Double by 2030

- Global data center power demand expected to almost double by 2030 | S&P Global

- Natural gas to play key role in strategy to double Canada’s electricity grid by 2050 | CBC News

- What to Know about Carney’s Plan to Boost Canada’s Electricity Output - Bloomberg