Strategic Asset Allocation – Why It Matters….

The Fortin Wealth Advisory Group - Jun 09, 2025

Well, these past few months were a ride weren’t they? I wanted to focus my writings this newsletter on taking it back to basics. We are called on by the affluent to manage investment portfolios with an elevated approach – similar to the way that institutions do – with a focus on preserving capital with growth that exceeds inflation and do so in a way that builds wealth for the next generations. The media, however, has all of their focus tied to day trading portfolios. What’s hot this week? Tech? Gold? Bitcoin? The media is similar to a mosquito in your bedroom at night… as Canadians I think we can all get behind that analogy.

Last year, the focus was Mag7, and absolutely we hold those companies in the portfolio, but not exclusively, that is just poor portfolio management. Although those specific companies crushed the S&P 500 last year, and we discussed with clients how frothy they were (which never lasts), they also got completely washed out as soon as some volatility came in. #asexpected

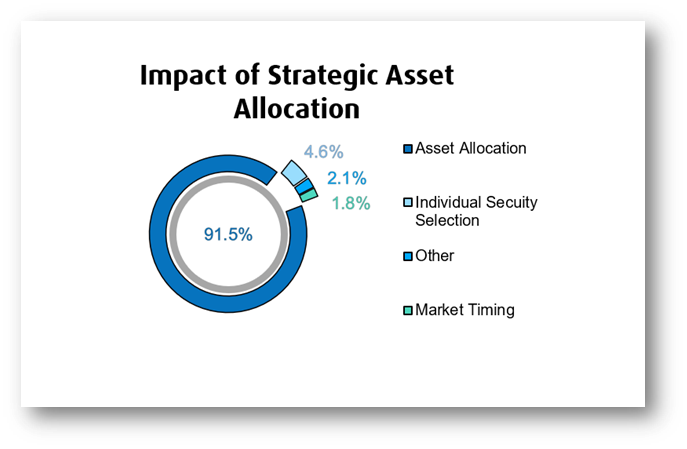

Enter, appropriate risk mitigation of portfolios with strategic asset allocation. There is a reason why our model portfolios significantly reduce the downside during periods of market correction – and that is because we are obsequiously devoted to quality money management. 92% of your returns are based on the appropriate mix of assets (including real estate and private equity) and only 8% of your returns are individual security selection. Put another way, 92% of your returns are getting the mix of US and Canadian and Mid Cap Global and Infrastructure and Small cap companies correct. And only 8% of your returns are due to picking let’s say Coca Cola v. Pepsi.

What is Brinson, Hood, and Beebower (BHB)?

Those of us Institutional Portfolio Management types, this is the foundation of constructing investment portfolios. Feel free to google and go down the rabbit hole, but in a nutshell, this was a highly influential study in 1986 and 1991 that was able to attribute returns into 3 buckets:

- Approximately 91.5% of the variation in portfolio returns over time is explained by getting the strategic asset allocation correct.

- Only 4.6% is attributed to security selection.

- 2.1% is attributed to other factors

- Only 1.8% is attributed to market timing (bonus 4th observation).

Source: Brinson, Singer & Beebower, Financial Analyst Journal, 1991

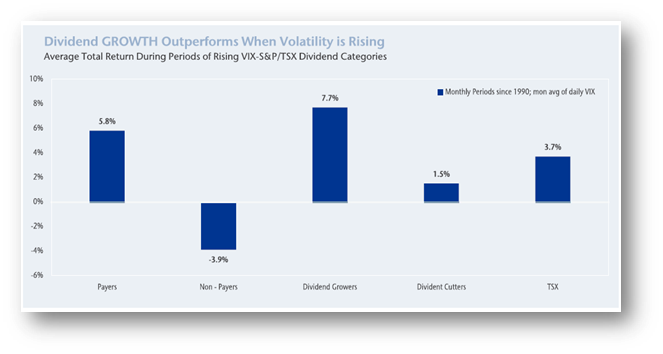

What saved our “Canadian” Bacon this year during the volatile times surrounding tariff talk? During initial unexpected shocks, there is very little difference that is made by asset allocation. Except for, if you were not diligent about re-balancing (think, owning a company that is going up in value and you just keep letting it go, instead of mindfully taking some profit off the table and re-allocating it to your fixed income component) whereby you suffered unnecessary losses. But, after the initial shock is through, companies that create ongoing value by increasing cash flow annually, and thereby growing their dividend perform better during volatile times. Your Mag 7 strict growth, have the worst performance as there is no compensation to hold on to them.

Source: Tamplin, T. (2024, January 25). Modern portfolio theory (MPT): Definition & how it works. Finance Strategists.

Strategic Asset Allocation is being “strategic”. Below you will find an article written by Ryan on Small and medium sized income paying companies, “small cap” for short. He will be speaking on when you see maximum divergence in valuation of larger and smaller companies which presents unique values. So, we utilize these periods of volatility to pro-actively manage our allocation. For instance, our small and mid cap companies provide the optimal risk adjusted return when they comprise of 30% of the Canadian equities against 70% in larger cap names. However, periods of volatility traditionally cause further declines in small and mid cap companies as retail investors flock to large banks. Thus, we will use that as an opportunity to take advantage of purchasing some excellently run companies that drive increasing EBITDA (earnings before interest and taxes) as discounted prices. Think, Neighbourly Pharma, Pet Valu, North West and AG Growth.

Source: BMO Capital Markets Investment Strategy Group, Factset, Compustat, IBES