2024 Fall Newsletter

The Fortin Wealth Advisory Group - Oct 11, 2024

We Are Living Longer – How Does That Change the Transition of Multi-Generational Wealth?

(World Economic Forum)

Fact: Life expectancy is increasing globally, which means people are living longer, and a 100-year life is not a realistic possibility for many.1

Fact: This could change the retirement age with people living a multistage life into their later years.1

Fact: The World Economic Forum and Mercer conducted a poll of people’s responses to living longer and both prospects for retirement in a new report.1

Fact: It found there’s a need for “longevity literacy” and an approach to wealth optimization plans that goes beyond financial security.1

For those of us who have worked with us for a long time, you know that the Wealth Optimization Journey and the ensuing Goals Based Report create the foundation for all subsequent tax, wealth creation, liquidity, estate, and insurance planning. 20 years ago, we used a mortality of 90 based on the actuarial tables when projecting out the implications of compounding tax requirements. I often would be respectfully challenged by clients on that number being too high. And while they observed the data that backed the number, they scoffed that it would apply to them.

Fast forward 20 years, and our wealth optimization plans routinely utilize a mortality of 98 years old. Further, it has changed the game of how we discuss the optimization of multi-generational family wealth.

In the days of old, it was ensuring that lifestyle expenses were covered. With a mortality below 90, the next generation would see the bulk of the assets transfer near the time of the next generation’s retirement thereby boosting their ability to retire as well as transfer some to 3G for asset purchases or educational needs. Now, if we use the same approach, 2G would be 80 years old, and 3G almost retired by the time assets are transferred.

The change in longevity is a complicated piece. We require more capital to cover living expenses, we are now causing larger tax liabilities the longer the assets are growing (especially with Family Trust and Corporate Structures), and arrangements for asset transfer need to be made 15 – 20 years before mortality to manage some of these complexities.

Given that Longevity Literacy is broadly under-discussed, here is my attempt to educate deeper on this topic.

What Excites You About Living Longer?

“The opportunity to see grandchildren grow to a more mature stage of their life than prior generations did. Retiring healthily enough to be engaged in my extended family’s lives; time to contribute to my local community.”

This was one of the responses to a Pulse Poll from Mercer and the World Economic Forum for their report Living Longer, Better: Understanding Longevity Literacy.2

A 100-year life is now within reach for many people, with children born today in middle-income countries having over a 50% chance of living for more than a century. 50% CHANCE!!! Life expectancy is increasing globally, according to the report. In the two decades between 2000 and 2019, it went from 66.8 to 73.4 years.3,4

Almost a third of the population of Japan (28%) is now aged over 65, while developing countries are expected to see a jump of 140% in over 65s by 2030, compared to 51% in more developed countries. Those additional years of life will require a different mindset to our later years, ensuring we’re maximizing our health and our chance at a healthy retirement.4

LIVING LONG, BETTER

The Pulse Poll found that while people value living longer, there are some genuine concerns. For instance, 40% want to have a better understanding of what their financial and tax situation throughout retirement may be. Only 45% feel they will be financially secure.2

Other concerns were health (43%) and then social inclusion and maintaining independence with dignity until the end of life were the ensuing categories of concern.2

Responding To Retirement Changes

The traditional three-stage life: education, career, retirement, is likely to become a “multistage life”, according to the report, with lifelong learning, career breaks, and new occupations built into later life.

Here are some of the key shifts in retirement and recommendations for what three critical stakeholders – government, the private sector, and individuals – can do to plan and respond accordingly.

Change 1: Health will become the top priority, so people can live longer, better lives!

What’s needed: Planning for good health will be even more critical, with individuals improving healthy life expectancy through good nutrition, exercise, and early screening, while governments can introduce health campaigns to increase “health span”. Employers can offer high-quality and more accessible advice about longevity and health.

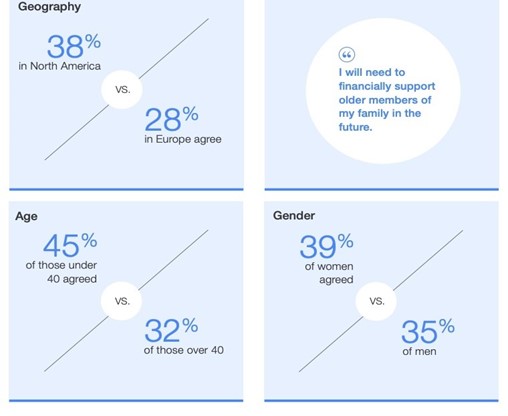

Change 2: Children are more likely to support parents.

What’s needed: The “Bank of Mum and Dad” may be closing, with 45% of under-40s expecting they will need to support elderly relatives, compared to 32% of those over that age. Governments can strategize to increase the caregiving workforce and improve the financial rewards, while businesses can provide flexible work programs and training for caregivers re-entering the workforce.3

Image: World Economic Forum

Change 3: Reskilling to work longer

What’s needed: With more than half of people either having not saved enough for retirement or unsure, many people will either need to accept a lower standard of living or work for longer. Reskilling will be required to keep skills relevant to the workforce, with governments driving upskilling efforts and discouraging ageism.

Change 4: Younger generations want to retire earlier – but may not have the funds

What’s needed: The Pulse Poll found 44% of under-40s wanted to retire by 60. More educational programs are needed from governments and employers to show the impact of different working arrangements and retirement ages on pay and pension. Auto-enroll pension schemes can ensure younger workers have more money saved.2

Source:

1. We’re living longer. Here’s how that will change retirement

2. Living Longer, Better: Understanding Longevity Literacy

3. Here's what young people think is key to a long and fulfilled life

4. GHE: Life expectancy and healthy life expectancy

10 Best Countries To Retire In

(According to International Living’ 2022 Retirement Index)

Their Survey included a combination of factors such as: cost of living, climate, quality healthcare, and how easy it is for foreigners to become permanent residents.

How Politics Affect Our Portfolios - Submitted by Ryan Lidder

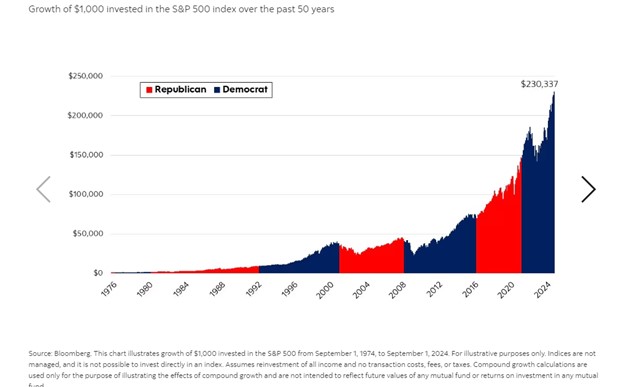

As we meet with clients and review our annual Wealth Plans one key question that continues to be a hot topic every four years is the impact of the U.S. election on portfolios. While it is an intriguing topic and one that can fuel conversation for an entire meeting end with a key take by Simon Sinek; “Leadership is not about the next election, its about the next generation”.

While elections bring short term volatility, it is important to emphasize the word short-term, as some stocks may see short term movements depending on the promises outlined by a presidential candidate. Underneath it all, a businesses true value is dependent on its overall fundamentals and not the party in power. Over the past 75 years we have seen a total of 18 presidential elections, with the U.S. market showing positive performance in 16 of those years. Leading up to election day market volatility tends to rise and has historically subsided immediate after, furthering the point of staying the course over the long-term is the correct strategy regardless of the electoral outcomes.1

An interesting example of this was seen in 2016 when most projected a Democratic victory and predicted a dire market should the Republications claim the victory. Looking forward a year, the unlikely outcome of a Republican victory had come true along with a 30% increase in the S&P 500 proving any short-term portfolio rebalancing to be costly.

While this may be only one recent example a look at the long-term trend proves that the market performance is rarely tied to the presidential outcome and more so to the current state of the economy as seen below over the last 50 years.

If not elections, then what moves the market?

Economic trends continue to be an important indicator for the financial markets and as we move closer to the end of 2024 both Canada and the U.S. are showing signs of economic strengths. Some key areas of focus continue to be:

- Inflation has significantly decreased.

- Consumer spending continues to be strong.

- Corporate earnings are robust, particularly among large-cap companies

- Economic growth has slowed but still surpassed expectations

- Additional monetary policy easing and rate cuts could further stimulate growth spending

As noted from Stephane Rochon of BMO Private Wealth Canada, “The economic cycle always trumps the political cycle.” And the present economic cycle continues to display durability as the unwinding of pandemic-era supply chain, employment, consumption, and production disruptions settle into new post-pandemic norms.2

Polices that help to provide support to the over economy come from fiscal policy moves such at decreases in interest rates to help support growth. High interest rates have been a key headline for the past two years and with The Bank of Canada, EU and now the U.S. Federal Reserve beginning their rate cutting paths we begin to see a strong case for continued economic strength.

In summary, keeping politics out of the portfolio has been a proven long term strategy as Trying to incorporate political outcomes into investment portfolios based on polling and predictions brings risks, but little benefit. Continual focus on long term economic trends coupled with companies that posses a strong balance sheet and long term business plan to success regardless off the changes in political power.

“The stock market goes up and down under every president, but the path of least resistance has always been higher.” - Danny Noonan, investment writer for Morningstar Investment Management

1. How do U.S elections affect stock market performance?

2. U.S. Election – Politics and your Portfolio – Carol Scheif BMO Private Wealth

Growing Our Team To Serve You Better

I am thrilled to announce that Dylan Joseph Farrago has joined the Fortin Wealth Advisory Group as our newest Client Service Associate.

Dylan was born on Long Island, New York, and lived there for 18 years. He moved to Vancouver with his family and attended the University of British Columbia to study engineering. Although Dylan enjoyed studying biomedical material engineering and obtained BASc, he eventually focused his efforts on transitioning into finance - recognizing his desire to support families with their wealth goals. And, his need to carry on complex discussions with the needs of Family Enterprises.

Dylan joins us from CIBC where he has put in time in the retail environment learning Wealth from the ground up and now will form part of our Service Team.

"I'm looking forward to forging my path with one of the most respected teams carrying some of the smartest advisors in the Wealth Advisory space."

- Dylan

In his free time, Dylan can be found either in the gym or watching football with his friends. While he enjoys playing various sports, Dylan is most excited to take his snowboard out and shred the slopes in the winter.

Introducing Our EARN Program

We are thrilled to announce the launch of our new financial literacy series, EARN – Educating and Assisting the Rising Next-Gen. Over the past two years, our team has worked diligently to develop a thoughtful and comprehensive program designed to provide invaluable guidance and support for the second and third generations of the families we serve. This series represents our ongoing commitment to ensuring long-term financial success and security for your family’s next-gen leaders.

As we introduce the first installment of the EARN series, we want to emphasize that this is just the beginning. We have dedicated considerable time to perfecting the best way to communicate these important principles. We are always available for personalized wealth counsel and EARN is meant to be a starting point to spark deeper conversations with the next generation. We will be uploading videos and articles that will help teach you about financial literacy. We want to be here to guide your family every step of the way.

ETFs and Mutual Funds… What’s The Difference?

Submitted by Jordan Goh

Meant for the next generation wealth leaders:

Exchange-traded funds (ETF) and Mutual funds are two different investments that are very common when building a portfolio. They may seem the same in many respects, but there are some differences that you should look out for.

Similarities:

Mutual funds and ETFs share similarities between them that may leave an investor wondering what the difference is between them.

Below are a few of the similarities between mutual funds and ETFs:

- Can both hold stocks, bonds, or commodities

- Can both track indexes

- Can both hold different investment objectives (Growth, Balanced, Income)

Both are great options for investors, however, there are some key differences to look out for between the two.

Differences:

Although Mutual Funds and ETFs seem the same, there are some differences that you may not know about.

Below are some of the differences between the two:

- You can buy or sell ETFs anytime during market hours, whereas mutual funds are traded once at the end of the day.

- ETFs are generally cheaper than mutual funds.

- The reason ETFs are cheaper is because Mutual Funds are often more actively managed than ETFs.

- Mutual Funds can sometimes have a minimum holding period. If liquidation occurs before this period is up, then there could be a penalty assessed upon redemption of the position.

- The initial investment for Mutual Funds is based on a dollar value rather than a share price.

- For ETFs, a taxable event will occur upon selling the share.

- Mutual Fund managers can distribute capital gains to investors, even if they are only just holding the position.

As a quick overview, ETFs and Mutual funds are two different investments that can be used to gain more diversification than investing in a single stock or bond. There are some similarities between the two, however the differences still need to be accounted for.

For more information, feel free to reach out to me directly and I can give more insight on this topic or any other questions you may have.

Source: ETF vs. Mutual Fund: What's the Difference?

Personal Note from Christine

Fortin Wealth is constantly looking to disrupt the status quo and stay ahead of the curve. On Thursday, October 24th the team had their 2nd out of the office Business Planning day for the year ahead. With an expanded team to serve clients better, much of the focus was on our Next Generation Programme, EARN, as we look to support new clients ages 30 – 45 for their early wealth planning needs to set them up for success.

As we brainstorm new ways of disrupting, we check in with you for a pulse check.

As you likely know, Christine has had a number of industry accolades but most important to her and Ryan is the opinion of our clients. Well, I am pleased to share that Fortin Wealth Advisory has been recognized by our firm as a top Wealth Counselling Team in the category of Client Loyalty and Satisfaction in a recent client survey.

The team placed in our top of almost 2000 Wealth Professional Teams allowing them to carry a Top in Client Loyalty recognition.

Receiving this recognition is an honour and that we are delivering a superior wealth management experience, making us the team of choice for Canada’s affluent families and their children.

If you were contacted for the survey and took the time to complete it, we want personally thank you for taking time to provide valuable feedback and for the continued trust you have placed in us your family’s financial needs. This survey is not the only opportunity to provide input on what is working well and what we can do better. Christine and Ryan are always available for these conversations.

Thank you for your business and loyalty.

Robin Esrock’s Bucket List

Fall 2024

Travel personality and bestselling author Robin Esrock has reported from over 120 countries on 7 continents. We’ve invited him to share travel inspiration.

GLOBAL DREAM FOR THE FALL: China’s Yellow Mountain

Fall foliage has burst into life across the northern hemisphere, attracting interest wherever leaves are turning. This season we’re off to one of the most famous mountains in China, a UNESCO World Heritage Site known for misty granite peaks, twisting pines, rich biodiversity and spiritual significance. Located outside of Huangshan City and accessible by high-speed train from Shanghai or Beijing, the Yellow Mountain has inspired millennia of art, music and poetry. Today, it offers gorgeous trails through dense forests of maple and pine, leading to teahouses, hotels, viewpoints and temples. A cable car shuttles visitors from the parking lot to the top, with trails catering to all levels of fitness. The cloud forests are particularly stunning in autumn, when it can feel like you’ve stumbled into a traditional Chinese painting.

CANADIAN DREAM FOR THE FALL: Ontario’s Agawa Canyon

Maple, birch, and aspen forests in Ontario are famous for their fall colours, and they meld together beautifully outside of Sault Ste. Marie. The Algoma Central Railway operates a scenic passenger train into a region made famous by various Group of Seven artists, who strived to capture its scenic beauty. The locomotive itself features large viewing windows, GPS-triggered tour narration available in five languages, and excellent dining. It's a full day adventure, lasting about 10 hours. Once you arrive at your destination of Canyon Park, you have ninety minutes to explore five easy walking trails, including a 76-metre-high canyon lookout. Budding photographers will be in their element, but the waterfalls, rivers, rock formations and magical fall foliage will appeal to everyone.

TIPS: Navigating Hurricane and Cyclone Season

Destructive storms are in the news, hitting the Atlantic and Pacific with alarming intensity, tearing through communities, and blowing vacations out the water too. The Atlantic hurricane season typically blows June 1 to November 30, peaking mid-August to late October. It impacts about a dozen US states - including Florida, Texas and as far north as New York - as well as many islands in the Caribbean, and Central America. The Eastern Pacific hurricane season is May to November, peaking July to September. This can hit the western coasts of Mexico, Central America, and occasionally California and Arizona too. Over in Asia, the Western Pacific typhoon season is most active May to October, peaking July to October, and impacting the west coast of Japan, China, Taiwan, Southeast Asia, and the Philippines. The North Indian Ocean cyclone season peaks May/June and October/November, bringing heavy rain and strong winds to the east coast of India, Sri Lanka, Myanmar, and occasionally the Maldives. If you’re planning a trip to islands in the South Pacific, be aware that January to March is peak cyclone season in that part of the world. Hurricanes and cyclones are rare but devastating, so if you are heading into their path during their peak season, carry cancellation travel insurance and keep an eye out for news and advisories.

LET’S GO: KAYAKING THE JOHNSTONE STRAIT

Next August, I’m delighted to host a one-of-a-kind tour in northern Vancouver Island that combines sea kayaking, immersive wildlife viewing, and an authentic Indigenous cultural experience. I’ll be the Canadian Geographic Travel Ambassador on karibu adventure’s special 6-day excursion, based out of Port Hardy and a comfortable base camp on the Johnstone Strait. This part of the world has been on my bucket list for years. It’s an opportunity to kayak among whales and other wildlife in a stunning region of B.C, while engaging with the history, art and traditions of the local Kwakwa̱ka̱’wakw people. No kayaking experience is necessary – it rates just a 2 out of 5 on the activity level - and the trip includes all meals, accommodation, presentations, and guided daily excursions. Click here for more details, I hope you can join me!

DON’T QUOTE ME:

“I haven’t been everywhere…but it’s on my list.” – Susan Sontag

If you have any travel-related questions or inquiries, feel free to email me at robin@robinesrock.com

Happenings

Christine has been keeping busy these past few months. On top of her regular working schedule, she had the opportunity to be a leader in one of BMO’s most impactful programs, The BMO Women in Wealth Mentorship program.

Christine is extraordinarily passionate about supporting the next generation of kick butt women wealth professionals. This program is focused on guiding mid career women to the top of their game.

It was a fantastic day of connecting with amazing Investment Professionals from across the country with the focus on mentorship, allyship, advocacy and talent development. To add icing on top of the cake, Christine has had the great pleasure and immense struggle of attempting a house move.

Unfortunately, we had to say goodbye to our summer intern Neelam this September. We wish her all the best in her future career. This is what she had to say “After four months it is a bittersweet moment to announce I have completed my internship at BMO Nesbitt Burns. My time at BMO has been full of an abundance of learning and self-development that I look forward to carrying with me into future endeavors. I am so grateful for the opportunity to have been given this experience and to have worked with such hardworking individuals.“

Over the summer, our team had an exciting break from the usual routine by participating in a fun-filled softball tournament at our BMO-wide work event. It was a great opportunity for our team to network and make new connections in the BMO family. The energy was high, and while we may not all be pros on the field, we brought our A-game and were able to finish in 2nd place!

Ryan had the opportunity to attend the Annual ICBA Construction Innovation Summit sitting with many of our industry leaders in the Construction industry and learning key business development ideas from the likes of David Robertson – Senior Lecturer of MIT School of Management and Billy Beane the legendary Oakland A’s Executive Vice President.

Its all about the kids in the Lidder household as Aanya learns to cook and baby Reyna plays pass with her favorite teddy bear.

Jordan headed down to Las Vegas for the Thanksgiving long weekend with friends. He was able to catch a Golden Knights game as well as a Cirque du Soleil show.

You all know that Kase plays football, this is his first year of playing tackle and he’s bringing the BOOM as a linebacker. When Kase isn't on the practicing on the gridiron, you can find him out fishing with the family.

More exciting news from the team:

We’re excited to celebrate a significant milestone for Jordan, who recently passed the LLQP: Life License Qualification Program. This accomplishment reflects his hard work ethic and drive to continuously learn. Dylan earned his Investment Representative license and has now begun participating in the Associate Wealth Advisor program. These will be a great additions to our teams’ capabilities and we look forward to seeing what Jordan and Dylan can achieve in the near future.