May 2026 Market Recap

Ashley Nichols - Jun 15, 2026

Curious why markets are thriving despite global uncertainty? This insightful update explores the resilience behind strong returns, the rise of AI-driven growth, and why staying invested—with a steady, disciplined approach—matters more than ever.

Money is a tool.

Money is a tool.

It's something that supports your life!

Portfolio Comment

Brent Joyce CFA;

Chief Investment Strategist and Managing Director, BMO Private Wealth

Goldilocks Held Hostage

"Economic progress, in capitalist society, means turmoil.”

– Joseph A. Schumpeter, 20th century economist, father of the theory of creative destruction

Three months after the eruption of hostilities in the Middle East, the most frequent question we get is, “Why are capital markets doing so well?” Year to date, the S&P/TSX and S&P 500 are up almost 10%, European markets are up mid-single-digit percentages, and Japan and emerging markets have climbed in the 20%-plus range.

The short answer: the global economy is less reliant on energy inputs today than it was in the past (and that’s not a too-distant past). In addition, the stock market includes many companies (very large and market-moving companies in technology and communications services) whose fortunes aren’t significantly impacted by a commodity shock.

In the early days of the conflict, the priority was to understand and quantify the effect of higher energy prices and other key commodity supply disruptions on the global economy, inflation, plus monetary and fiscal policy, and evaluate their implications for equity and bond markets worldwide.

Three months on, we see our view was directionally correct; however, we didn’t appreciate how much the positives we outlined are canceling out the negatives. Investors are reminded that during times of uncertainty it’s important to remain calm, focus on the facts, and stay invested.

We now see that the economy has enough momentum to absorb this shock and still be okay. Prior to the shock, the economy was unfolding along the Goldilocks theme – not too hot and not too cold. Today, Goldilocks is being held hostage in the Strait of Hormuz, but she can be freed.

Priced to pass

Middle East supply disruptions are being managed in a number of ways: through some demand destruction (like work-from-home mandates/guidance in some countries); rerouting around the Strait of Hormuz (SoH); clandestine shipping; relaxed sanctions against Russia; increased production elsewhere; and the use of strategic inventories.

Providing additional salve for the capital markets: prices for key commodities in futures markets are still signaling that the conflict will be resolved – oil contracts for delivery in one, two and three years are all in the US$70 range (and have stayed there despite the on-off ceasefire/SoH reopening promises).

The economy’s ability to continue absorbing the shock may have an expiration date, but that date appears to be much farther down the road than many had imagined.

In the meantime, positive drivers of stocks and certain parts of the economy have picked up the slack (capital spending on defense, infrastructure, and AI). Softening the blow are previously announced tax cuts – including tax cuts on energy specifically – and consumers who are dipping into their savings (not a long-term positive factor).

When Goldilocks does eventually break out, we’ll need to be vigilant. Given how strong the economy remained while still shackled by fallout from the war, there is a risk the economy could run too hot. The easing of Middle East hostilities would see energy prices retreat, but the spending on defense, infrastructure, and AI innovation could prove inflationary in the near term.

Inflation is unfair, the market doesn’t care

Inflation is perking up; however, recall that it was on a downward trajectory pre-conflict. In addition, some of the things causing that downward trend don’t respond quickly to a commodity shock – housing and wages, to name two.

We aren’t dismissing inflation; it is a problem. Inflation running a little high (the number starts with a three instead of a two) is problematic, especially for the lower echelons of the economic strata. Cold and calculating capitalism doesn’t react to this plight until things start to break – unemployment rises or consumption falters more broadly beyond the bottom of the so-called K-shaped economy (some call it E-shaped – a top, middle and bottom). Either way, escalating inflation and higher short-term borrowing costs and mortgage rates aren’t meaningfully crimping consumption or employment. Therefore, policymakers, both fiscal and monetary, are not panicking. Rumblings from these quarters did drive some volatility in bond markets during the month. The whole issue of potential central bank actions (either raising or lowering rates) remains a top worry for some market pundits. We are not among them.

Not convinced rate hikes are coming

While we believe central bankers are loath to raise rates, circumstances may force them to act. If central bankers do raise rates, we think it will be motivated more by their desire to maintain credibility and less about the impact one or two rate hikes will have on the economy (it certainly won’t fix the supply-side constraints).

Although rate hikes are not constructive in our opinion, we also don’t believe hikes (even if they are motivated by central bankers’ desire to maintain credibility) will upset the apple cart; markets respond to rate cycles, not minor tinkering.

Markets don’t get too fussed about central banks changing rates in either direction unless bankers signal that these moves are the start of a sustained campaign. We aren’t hearing this, nor are markets pricing in this scenario. We are cognizant that this scenario could happen, yet we believe it is far enough down the road that we can put it in the “on watch” category for now.

Credibility-driven hikes can indicate that central bankers aren’t ignoring the inflation bump. This could result in higher shorter-term interest rates; on the other hand, mid-and-longer term bond yields may stabilize or even fall slightly.

The stock market isn’t the economy

Equity markets are driven by a variety of factors. While broad economic growth is one important ingredient, it isn’t the only one – equity markets are also where innovation is funded and rewarded.

What we have is a decent traditional economy in the world’s largest market (the U.S.), and in many other places economic growth is hanging in. At the same time, the innovation story (all things AI) isn’t particularly beholden to oil or the consumer (yet).

AI is still in the buildout, capital-expenditure stage. In some respects, it is still in the discovery phase, too, as it continues to deliver surprises. For investors, the best surprise is spectacular earnings growth, and the spread of that earnings growth to more companies. The most recent example is increased sales and revenue at an expanded set of semiconductor companies.

Time will tell if the exponential acceleration in some of these share prices represents a bubble. If it turns out to be a bubble, we currently see it limited to these select companies. We remind investors that neither these companies nor these sectors represent the entirety of the equity market’s opportunity set. We remain vigilant for extreme bubble behaviour.

It’s all about earnings, always

Ultimately, equities have enjoyed surprisingly good results because earnings growth has been surprisingly stellar.

Some criticize that aggregate earnings of a benchmark index are skewed by the massive amounts of spending happening in the AI rush. Skewed doesn’t mean weakness is masked in all other sectors. Earnings growth is simply good to better at many companies and spectacular in some AI-related areas.

Across the globe, estimates are rising for earnings growth. Yes, the biggest bumps are in the AI-related businesses, but it isn’t all AI. Supportive earnings growth is broad based. Consider Canada, where all 11 S&P/TSX sectors saw sales growth; seven sectors posted positive earnings growth, while six logged double-digit growth.

For the S&P 500, it was almost a clean sweep: 11 of 11 sectors delivered sales growth and 10 of 11 posted positive earnings. Consider that over half of the S&P 500 companies reported year-over-year earnings growth of 10% or more. Half of these, 128 companies, grew earnings by 25% or more.

Earnings are the lifeblood of share-price growth – and the earnings are delivering. AI juiced, yes; the whole story, no.

Investment strategy

We favour equities over fixed income. Equities are the preferred asset class barring a growth slowdown or recession – neither is our base case.

Our equity overweight is expressed in Canadian and U.S. equities and a neutral target for international developed markets (EAFE) and emerging market equities.

Our overweight to Canada provides exposure to energy and other commodities as a hedge. We caution that year-to-date gains of 30% in the energy sector are at risk of a pullback if the Middle East conflict eases. Overall well-diversified exposure handles this risk.

healthy sector rotation has played out within U.S. equities more than once throughout this bull market. The largest companies, mostly tied to the buildout of AI (Magnificent Seven, hyperscalers, semiconductors, and software) have raced ahead and faced scrutiny where share prices have come under pressure. U.S. equities have demonstrated resilience during these “tests” as other sectors of the market and smaller market capitalizations took up the leadership baton. An opportunity remains for this to continue, and we see better valuations in the broader market – for example, the equal-weight S&P 500 is not as expensive as the market-cap-weighted version. We continue to favour small and medium-sized companies to take advantage of this opportunity.

More growth-oriented investors should consider exposure to emerging markets. Emerging markets feature strong expectations for earnings growth, cyclical orientation, benefit from U.S. dollar weakness and sit at more reasonable valuations.

We see conditions conducive to equities outperforming fixed income. Nevertheless, there are downside risks. Excessive equity market exuberance is on our radar. Valuations aren’t extreme across the board, but a lot of good news is already embedded in prices. Risks re geopolitics, tariffs and inflation remain. A disappointment in economic growth, earnings growth or profit margins could bring a setback for stocks.

The Last Word: Innovation is productivity and progress

Since the 17th century when the Dutch invented stock markets, their function has been to connect those who have excess savings (investors) to those who need capital (entrepreneurs). Innovations require capital. Occasionally, new broad-based, general-purpose technologies have a wide impact on society and equity markets.

AI is considered a general-purpose technology (or GPT, not to be confused with GPT in ChatGPT which is Generative Pre-trained Transformer). The test of whether AI is a revolutionary GPT is playing out. The daisy chain goes like this: inventions need capital, stock and bond markets (hence the term capital markets) provide that capital.

In the meantime, the invention gets built out and winners and losers are identified while companies race to be the first, fastest, best, most-adopted owner of the technology.

By definition, if it is a true GPT, the technology is productivity enhancing and many other companies outside of the initial ecosystem will begin to adopt it. This adoption leads to productivity gains across a widening swath of the economy.

Even though there are disruptions, trade-offs and growing pains, productivity has historically and always been a powerful driver of rising standards of living, and a larger economic pie. The first slice of that pie goes to the innovators (i.e., huge single-stock gains and mammoth companies that didn’t previously exist). The second slice goes to the providers of capital more broadly as share prices rise across industries on productivity gains. Lastly, the many remaining slices go to society more broadly.

Every technological advance has generated fear of change to the status quo and anxiety about what the new will look like. We know humans by nature are wary of change. Yet, we also know that technology is just a tool.

Modern society would be much less enjoyable and prosperous if we still used the sickle and hoe, the buggy whip, or that corded landline phone on the kitchen wall. As Dr. Schumpeter reminds us, economic progress requires some turmoil.

Our Portfolio Management Approach

We are fundamental investors that use technical analysis to manage short-term market risks. We believe that risk management is not a choice, but a necessity. While we cannot control how much downside the market provides during a correction, we can control how much of the downside your account receives. We aim to avoid 60% or more of the decline in any significant downturn. Without our process, there is a good chance you will experience 100% of the downside from the market. We will help you navigate the risks and rewards of the market so that you can stop worrying about your money and start living your life.

Stay tuned for a new episode of "Why Do We Do That?" this month!

Transactions

The following is a chronological list of the trades:

We added to our Magna holding to make it a full position.

Established an initial position in Magna

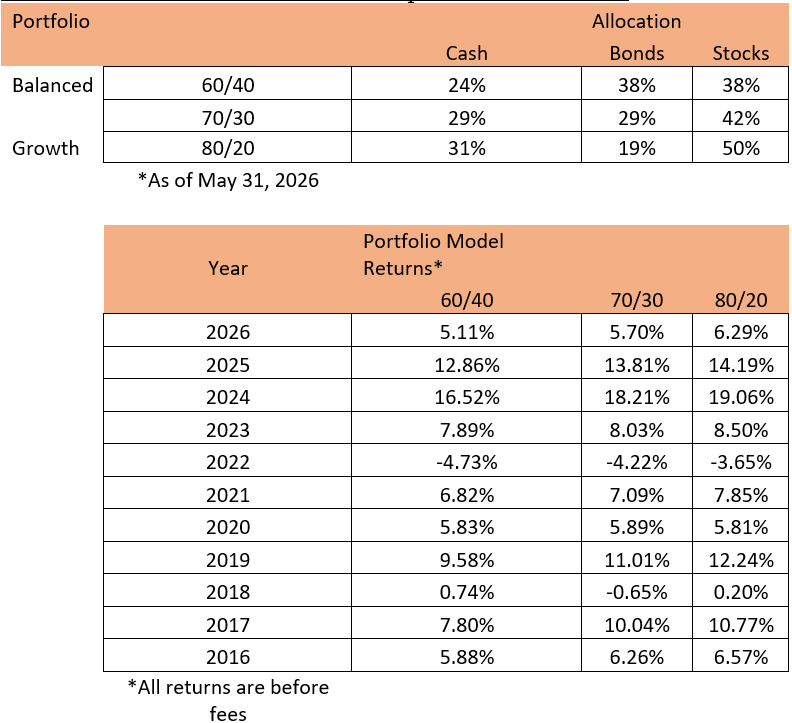

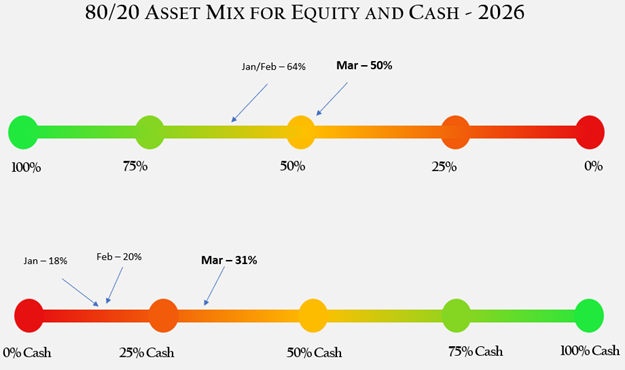

We are currently sitting with around 30% cash,

We are looking to add to positions.

Returns on our 60/40, 70/30 & 80/20 portfolios, before fees:

Interesting Charts

Technical Comments

Market Overview: S&P 500 E-mini Futures

The market formed consecutive strong monthly E-mini bull bars, breaking into new all-time highs. Bulls want a measured move to around 8000 based on the height of the April spike bar. Bears want a failed breakout above the bull trend channel line within a few months, followed by a retest of the bull trend line.

- May formed a follow-through bull bar, closing near its high.

- Last month, we said traders would watch whether bulls could create follow-through buying and, if the market broke above the bull trend channel line, whether the move would be sustainable or lack follow-through buying.

- The market traded higher, closing above the trend channel line and into new all-time high territory.

- Bulls achieved the measured move to 7550 based on the height of the prior trading range.

- Next, bulls want a measured move to around 8000 based on the height of the April spike bar.

- Bulls want any pullback to be weak and sideways, forming prominent lower tails.

- Bears want a failed breakout above the bull trend channel line within a few months, followed by a retest of the bull trend line.

- They see the current move as part of a climactic rally late in a trend.

- Bears need to create strong bear bars or candlesticks with long upper tails, closing below the middle of their ranges to indicate strength.

- If the market continues higher, bears hope it will form a blow-off top followed by a deep pullback in the months ahead.

- The market pulled back to the 20-month EMA in March and then rallied strongly into new all-time high territory.

- The May monthly candlestick closed near its high, increasing the odds of at least slightly higher prices in June.

- The market could gap up next week. Small gaps often close early.

- Big bull bars late in a trend can be part of a buy climax.

- Consecutive bull bars closing near their highs indicate bullish strength.

- A strong momentum move such as this can last longer than traders expect and sometimes ends in a parabolic buy climax or a blow-off top.

- Traders will watch whether bulls can create follow-through buying in June to test near the 8000 measured move target.

- Or whether the market trades higher but starts forming candlesticks with prominent upper tails, closing below the middle of their ranges, or bear bodies instead.

- Breakouts above or below trend channel lines typically fail within 2–5 bars (months)

Millennial Minute

The best defence against fraud is knowing how to spot it. Scams continue to increase, and investors fall for them every day.

This month’s article gives some insight into the different types of fraud you could face as an investor.

Click here to read!

Planning Article

Risk Management for Retirees: When to Reduce Exposure

Retirement is typically when life frees up and you have more freedom to explore all of the things you've been planning to do once the work stops. It can put a damper on things when you're constantly worried about your portfolio's protection against market volatility.

Although retirement means winding down your savings while you enjoy the golden years, it can cause a lot of retirees anxiety to see the numbers on their statements get lower.

Talking with your advisor about reducing your risk exposure might help you regain your peace of mind.

Click here to read!

DISCLAIMER:

The opinions, estimates and projections contained herein are those of the author as of the date hereof and are subject to change without notice and may not reflect those of BMO Nesbitt Burns Inc. (\"BMO NBI\"). Every effort has been made to ensure that the contents have been compiled or derived from sources believed to be reliable and contain information and opinions that are accurate and complete. Information may be available to BMO NBI or its affiliates that is not reflected herein. However, neither the author nor BMO NBI makes any representation or warranty, express or implied, in respect thereof, takes any responsibility for any errors or omissions which may be contained herein or accepts any liability whatsoever for any loss arising from any use of or reliance on this report or its contents. This report is not to be construed as an offer to sell or a solicitation for or an offer to buy any securities. BMO NBI, its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities mentioned herein as principal or agent. BMO NBI -will buy from or sell to customers securities of issuers mentioned herein on a principal basis. BMO NBI, its affiliates, officers, directors or employees may have a long or short position in the securities discussed herein, related securities or in options, futures or other derivative instruments based thereon. BMO NBI or its affiliates may act as financial advisor and/or underwriter for the issuers mentioned herein and may receive remuneration for same. A significant lending relationship may exist between Bank of Montreal, or its affiliates, and certain of the issuers mentioned herein. BMO NBI is a wholly owned subsidiary of Bank of Montreal. Any U.S. person wishing to effect transactions in any security discussed herein should do so through BMO Nesbitt Burns Corp. Member-Canadian Investor Protection Fund.

BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.