February Market Update

Ashley Nichols - Mar 16, 2026

Our monthly recap of the market is ready, and we share an article regarding the war in Iran and the implications it could have in certain market sectors. We share our performance numbers, tax tips for investors and new scams to watch out for!

Money is a tool. It's something that supports your life!

Money is a tool. It's something that supports your life!

Portfolio Management Comment

Iran Update

Mark Bayko, Head North American Equities

Brent Joyce, CFA, Chief Investment Strategist

Dan Phillips, CFA, Chief Investment Officer, U.S.

Carol Schleif, CFA, Chief Market Strategist

“Markets don’t fear war. They fear uncertainty."

– widely held investment aphorism

The Through Line: Capital markets have a long history of looking past geopolitical events. An initial (and often sharp) risk-off reaction is typically followed by recovery as investors return to focusing on fundamentals. Sorting the intermediate- and longer-term implications of the current Middle East conflict will take time and nuance as investors process the implication for energy markets, inflation/interest rates and investor sentiment. We remind investors that global economies were in very solid shape heading into this event, and markets (both risk and defensive assets) had arguably been positioning themselves for weeks.

Escalating conflict in the Middle East

The military engagement between the U.S., Israel and Iran has intensified in recent days as other countries have become

embroiled in the conflict. Attacks on military bases, embassies and energy infrastructure across the region have escalated – despite the disablement of substantial portions of Iran’s military capability. Threats to shipping continuity through the Strait of Hormuz have also been top of mind. After initially absorbing the news of the

conflict with steady trading on Monday, markets subsequently shifted to more intense concern. Investors hate unknowns – and the duration and potential off ramps to events seem murkier than they did over the weekend when a quick resolution was the hope.

Investors focused on oil

For the Middle East, the obvious transmission mechanism is through oil prices. Back in December they were at their lowest level in five years but have been rising in 2026 on expectations of stronger global growth as well as in the wake of the breakout of Iranian hostilities. Investors are focused on the Strait of Hormuz, an important choke point through which ~20% of global seaborn oil and liquified natural gas passes. Iran has announced the Strait is closed and has threatened any ships that attempt to pass through, though details have been changing as the situation is very fluid. Insurers have significantly increased pricing – or entirely dropped coverage – and invoked war time clauses for vessels contemplating passage through the Strait, causing many to drop anchor. If oil can’t get out of surrounding countries, a “shut in” process starts whereby production activities are stopped due to lack of additional storage.

The world has navigated oil shocks in the past, most recently with the war in Ukraine and last year’s 12 day Iran war. It’s

important to remember that prior oil shocks happened when the U.S. was a net importer of oil and gas versus the current

position as a net exporter. Canada’s position as a net oil exporter also helps mitigate direct economic implications – though both countries are obviously troubled by the overall increase in prices.

The reaction in the oil markets is to be expected and the magnitude of the move is manageable (for now). Then too, the world was actually estimated to have entered this conflict with a surplus of oil, with some estimates placing it at over 1 billion barrels. The issue, of course, is getting it where it needs to go without significantly raising prices/extending timelines. Notably, there are strategic reserves in many countries including the US, Japan, Europe and China. Oil will continue to be volatile, but a short-term spike doesn’t threaten the fundamentals markets care about most – which is the solid trajectory of global growth and in turn, corporate earnings.

Potential economic impacts

Inflation – higher energy prices, if sustained, could impact prices at the pump and theoretically pass through headline

inflation until resolved. We would expect the Fed to look through such an outcome given the supply/demand dynamics

of U.S. sourcing. There are plenty of deflationary tailwinds (softer hiring/wage growth and deflationary impact of

technological advances) that are keeping a lid on rates. The flight to sovereign yields as haven assets is putting downward

pressure on interest rates. The U.S. navy has substantial assets in the area. The Administration could deploy them at any time to help accompany shipments through the straights to keep the shipping and supply chains functioning.

Impact on China – The threat to energy markets (first via Venezuela, now Iran) is a not-so-subtle message to China that

the U.S. holds sway over key sources of China’s energy. China imports huge amounts of cheap fuel to sustain its low-cost

manufacturing infrastructure from those partners (as does India). Recent developments could have a notable near-term impact on China’s economy given its manufacturing infrastructure’s dependence upon cheap oil imports. Iran and Venezuela were not only two of China’s key allies/proxies - but were also providing ~20% of their oil supplies (much at discounted prices). Meanwhile, Russia is currently providing an additional ~20% of China’s oil supplies (also at discounted prices) - oil that could potentially return to the open markets as part of any peace deal. China would still be able to access necessary supplies, but would lose the discounts they have enjoyed.

Market impact

Equity markets came into this period within just a few percent of all-time highs, though significant internal rotation had

been occurring as the hand off of current tech-focused/narrow leadership to a broader cast of participants took place. While a potential for conflict had been expected (as naval assets were shifted into the area) this churning beneath the surface that otherwise represents a healthy rotation can leave markets on edge and with an uneasiness that can exacerbate reactions.

Haven assets – Gold, treasuries and most significantly the U.S. dollar – have rallied in recent weeks and are currently holding steady. This is constructive and reinforces a key fact we’ve stressed all year: markets are functioning exceedingly well – as are the underlying economic fundamentals.

Markets (especially stocks) tend to look through wars relatively quickly, returning focus to fundamentals. And the fundamentals remain sound - for the U.S. and global economies and for companies. For example, in the nearly finished 4Q 2025 reporting season with 99% of company results in, aggregate S&P 500 revenue growth was 10% with 15% earnings growth.

Implications for Investors

Once past the near-term volatility, we believe the economic expansion and associated equity-bull market should remain

intact. There is the possibility that the weakening of the Iranian regime brings less instability to the region - a positive outcome for global growth and oil prices – and hopefully for the people of the Middle East as well.

We reiterate our view that global economies are teed up for solid growth in the year ahead. Pro-fiscal stimulus politicians

have been voted into power in key countries and infrastructure and defense spending plans are increasing accordingly. Markets have absorbed well the many challenges thrown at them in the past 18 months and we expect the current situation to be similar. Exposure across a variety of global equity markets and sectors, with bonds playing an important cushioning role continues to show diversification works.

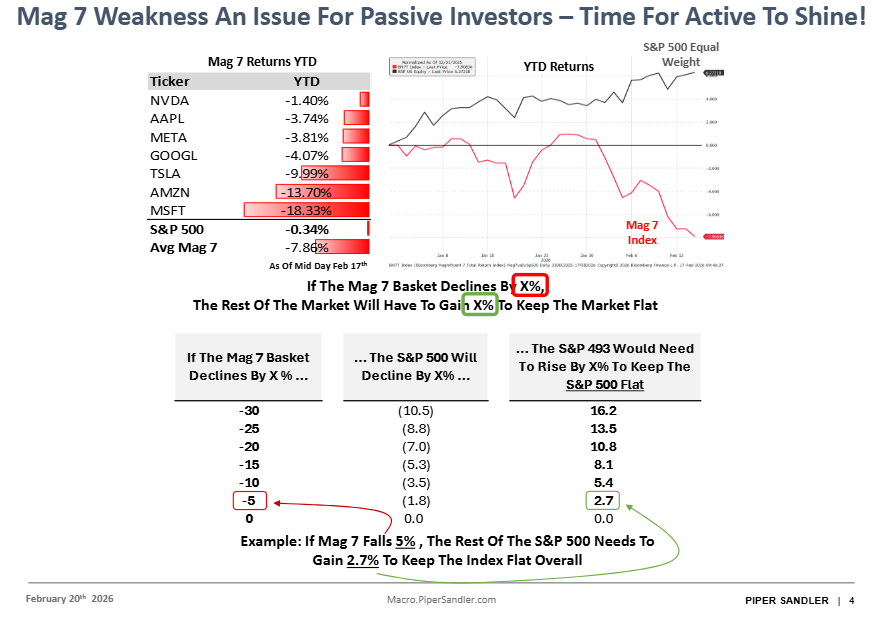

As we started 2026, market participants were highly attentive to signs of a market bubble. Such fears have been pushed to the back burner, thanks to recent volatility – even though many global bourses are at or close to all time highs. Though the broader indexes are up for the year, there has been substantial divergence under the hood as previous leaders (Mag 7 and other mega-cap tech) hand leadership to a broader constituency. This is indicative of healthy market function and helps set the stage for continued durable (albeit with continued volatility) action.

The growth phase in the global economy is not over. In fact many pieces are in place that argue for even sturdier growth. Newly elected legislators in many key geographies have a mandate to increase fiscal stimulus, military/infrastructure spend and/or cut taxes. Global trade is rebalancing as new supply chains and trading agreements and regional consumer blocs are hammered out. The TINA (there is no alternative) and FOMO (fear of missing out) mantras that directed investment activity primarily into U.S. assets is broadening, leading to more diversified global flows and a growing pie for more to partake of. Traditionally, the unwind of growth phases tends to come when leverage is applied and incentives go awry. We’re not there yet. With stocks near all time highs, consider rebalancing into other locales, sectors and/or market cap ranges as volatility allows.

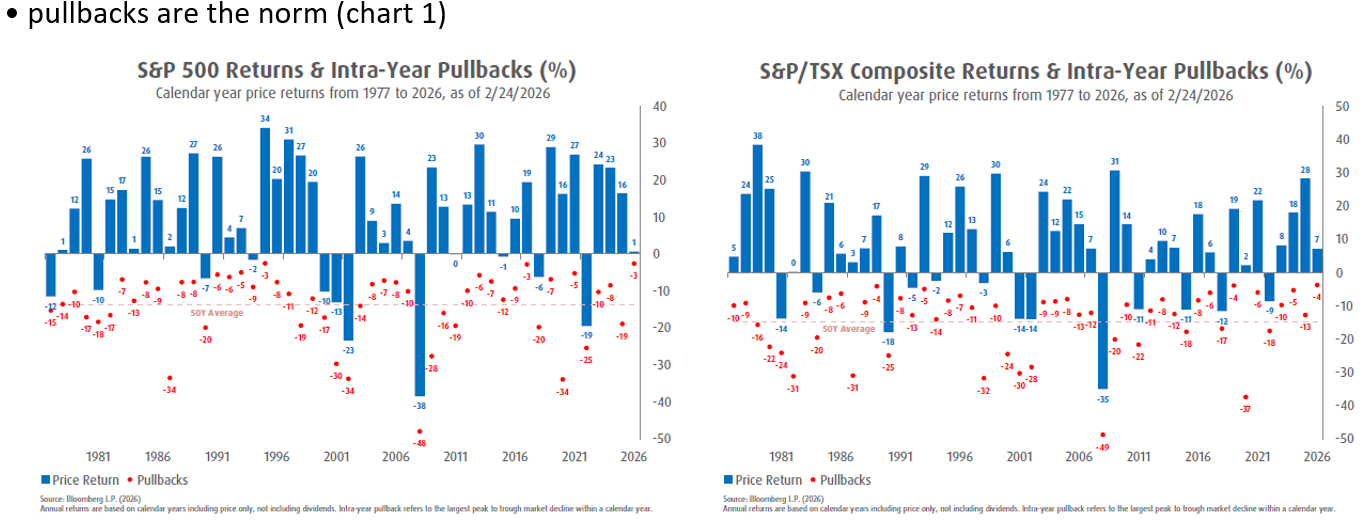

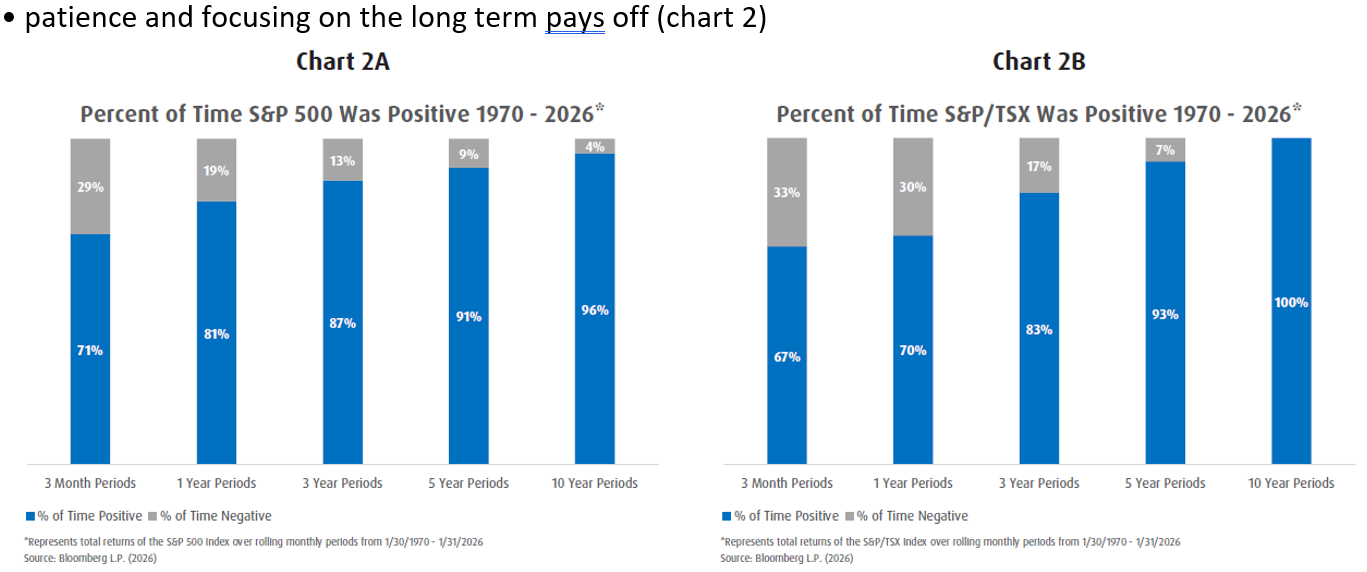

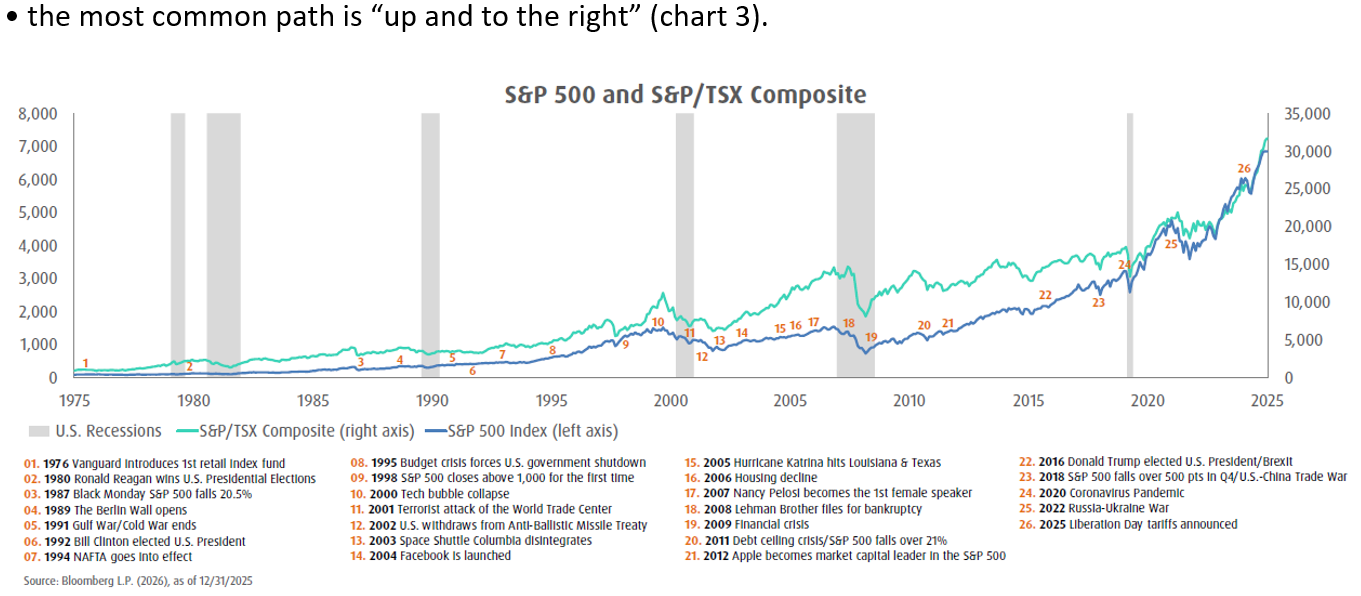

Bottom line: volatility-induced reboots are not fun – but they are healthy indicators of well-functioning markets, provided fundamentals remain intact. They also can grant patient investors the opportunity to benefit from the impetuousness of less patient investors.

Our Portfolio Management Approach

We are fundamental investors that use technical analysis to manage short-term market risks. We believe that risk management is not a choice, but a necessity. While we cannot control how much downside the market provides during a correction, we can control how much of the downside your account receives. We aim to avoid 60% or more of the decline in any significant downturn. Without our process, there is a good chance you will experience 100% of the downside from the market. We will help you navigate the risks and rewards of the market so that you can stop worrying about your money and start living your life.

Transactions

The following is a chronological list of the trades:

- The tactical trade that was executed on the QQQ did not hit our target and was closed out.

- We bought the ZQQ at $177.84 and sold it at $168.25

- We sold Cencora as it was looking very extended. I was purchased at $220.92 and sold for $360.135

- We also sold Mastercard at $541.17 after buying it for $465.58

- We sold intact Financial for $264.30 after buying it at $257.40

The proceeds of these sales were directed into 2 new holdings.

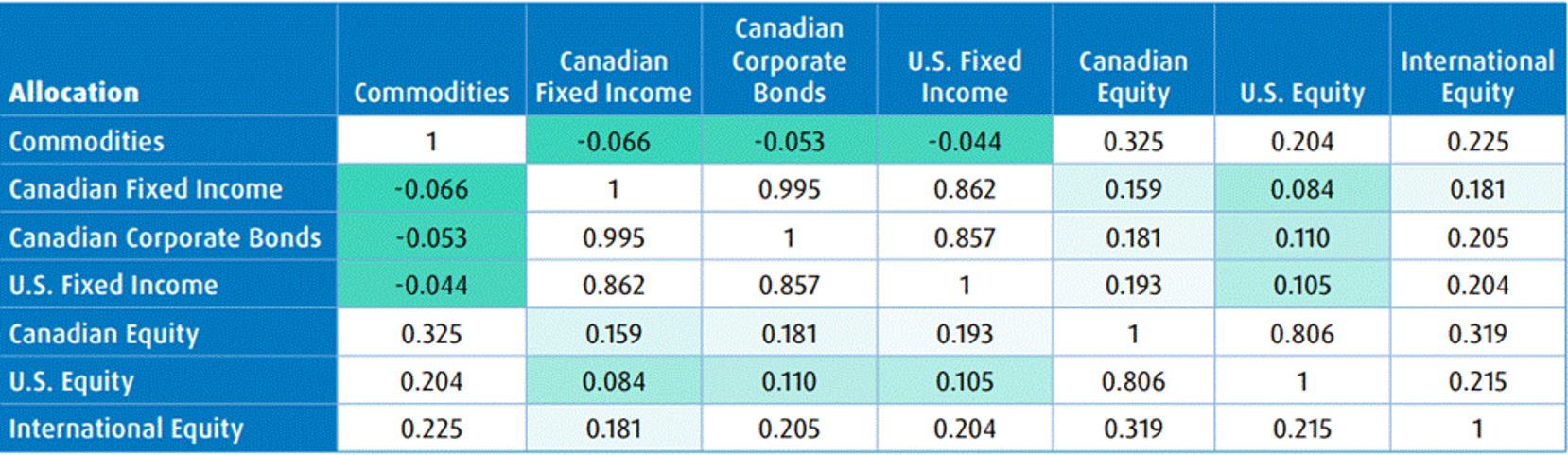

ZCOM – BMO Broad Commodity ETF (5% position)

ZCOM is a Canadian‑domiciled exchange‑traded fund that seeks to replicate the total return of the Bloomberg Commodity Index Total Return, net of fees. The ETF provides diversified exposure across major commodity sectors, including energy, agriculture, precious metals, industrial metals, and livestock. Exposure is achieved primarily through derivative instruments rather than physical holdings.

Enhance portfolio resilience with diversification

- Commodities have shown low to negative correlation with stocks and bonds

Inflation Hedge

- Commodities can help protect your purchasing power during inflationary times

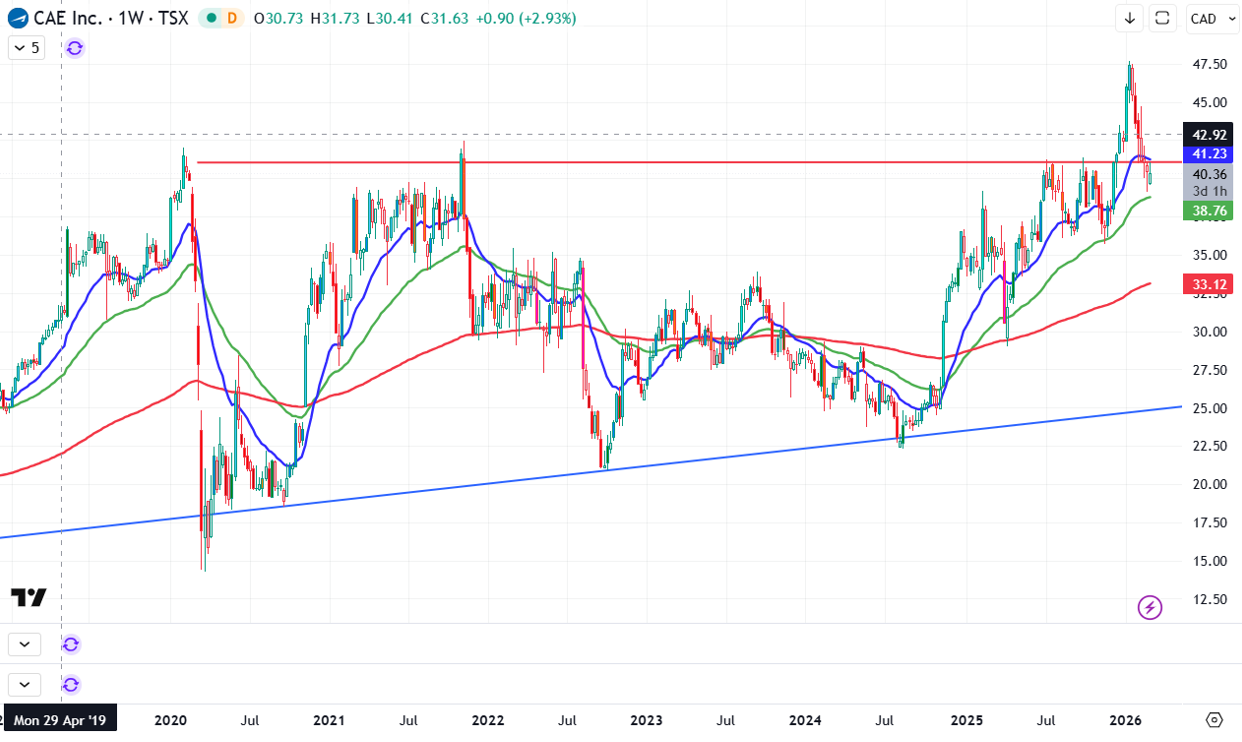

CAE Inc.

CAE is the global leader in aviation training and simulation, serving both civil aviation and defense & security customers. The company operates in over 40 countries with ~240 training locations, making it extremely difficult for competitors to replicate its scale, regulatory approvals, and embedded customer relationships.

Training is mission‑critical but non‑discretionary: airlines and militaries cannot operate without certified pilots and crews, regardless of economic cycles. This gives CAE strong pricing power, high customer switching costs, and recurring revenue characteristics.

CAE ended Q3 FY2025 with a record adjusted backlog of ~$20 billion, providing multi‑year revenue visibility and reducing earnings volatility.

- Civil Aviation backlog: ~$8.8B (+44% YoY)

- Defense & Security backlog: ~$11.5B (+100%+ YoY)

Backlog growth has been supported by book‑to‑sales ratios well above 1.0, signaling continued future growth rather than backlog erosion.

Improving execution and financial discipline:

Research highlights a clear management‑led transformation focused on improving financial outcomes rather than just revenue growth. Key priorities include:

- Portfolio optimization and balance sheet improvement

- Stronger capital discipline with emphasis on ROIC

- Better asset utilization within the Civil training network

Management’s increasing focus on free cash flow generation and capital efficiency is viewed as a key driver of long‑term value creation.

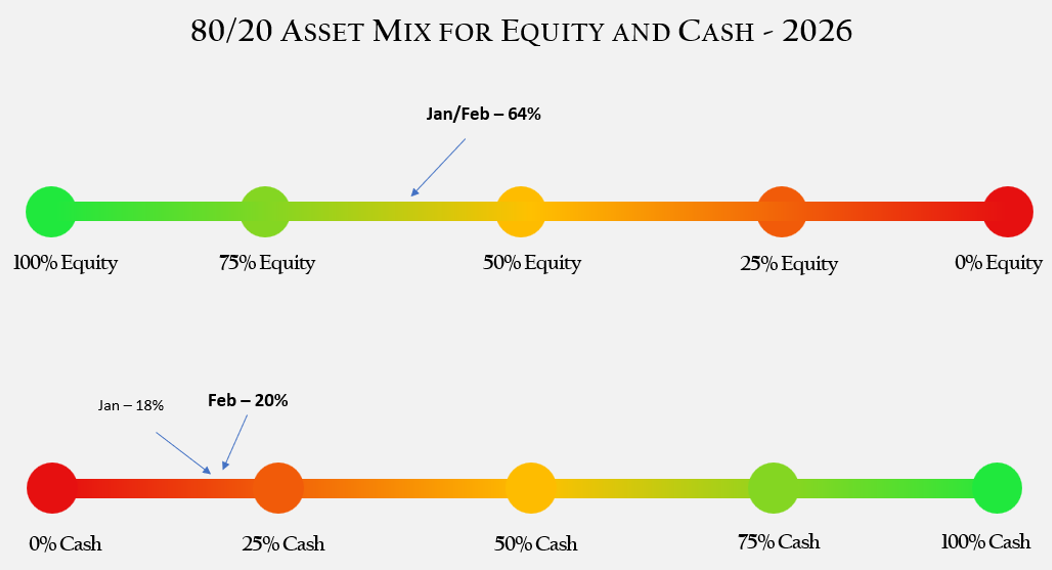

We are currently sitting with around 20% cash. Looking to add to positions during any pullback in March.

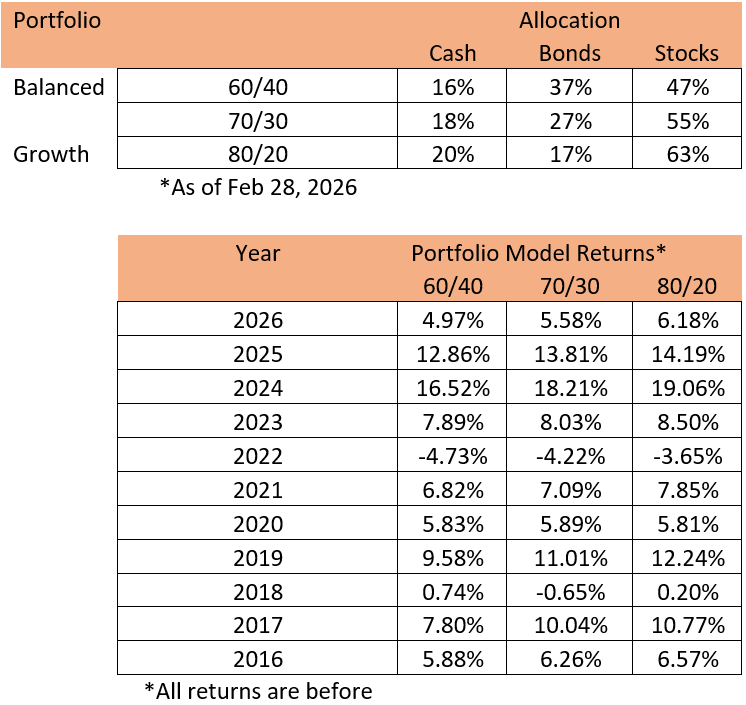

Returns on our 60/40, 70/30 & 80/20 portfolios, before fees:

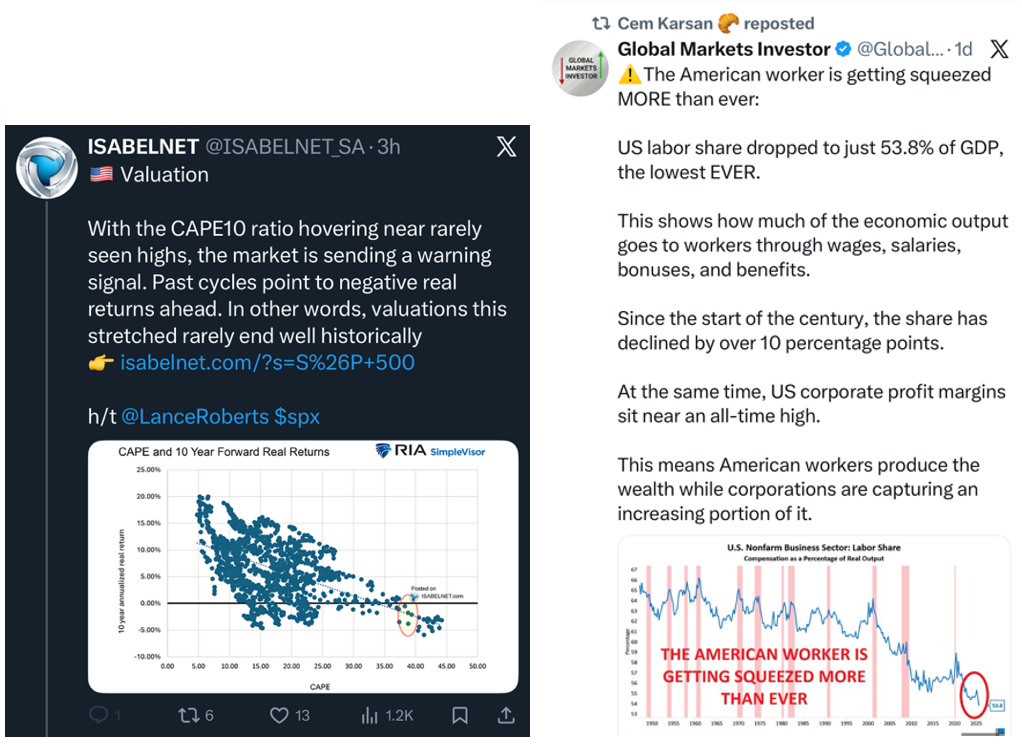

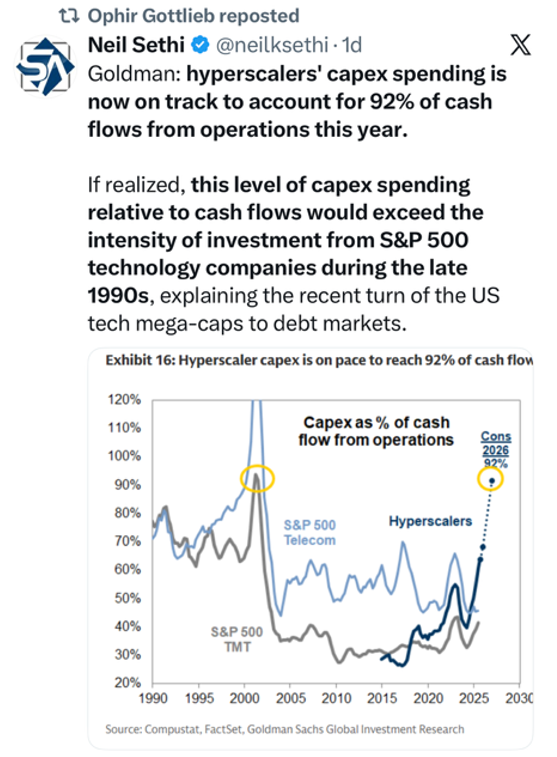

Interesting Charts

Technical Comments

Monthly E-mini Tight Trading Range | Brooks Trading Course

The market formed a monthly E-mini tight trading range near the all-time high. Four consecutive dojis signal temporary balance between bulls and bears. Traders will watch for a breakout in either direction and, more importantly, the strength of follow-through.

The Monthly E-mini Chart

- February formed a bear doji closing near the middle of its range, with a prominent lower tail.

- Last month, we said traders would watch whether bulls could break above the sideways trading range with follow-through buying, or whether the market would continue to stall near the all-time high and pull back in the months ahead.

- So far, price continues to consolidate sideways near the all-time high.

- Bulls need a strong breakout above the January 28 high with consecutive bull bars to resume the trend.

- They are targeting a measured move to 7,300, based on the height of the recent tight trading range.

- If the market trades lower, bulls want the December or November lows to hold as support, forming a higher low and a double bottom bull flag with the November low.

- Bears want a reversal from a large wedge pattern (July 27, December 6, and October 29) and a small double top (October 29 and January 28).

- The recent sideways overlapping candlesticks indicate bears have caught up to prior bulls’ strength.

- Bears need a strong breakout below the tight trading range with follow-through selling to increase the odds of a successful reversal.

- Bears want a measured move toward 6,500, based on the height of the 3-month tight trading range.

- If price breaks above the all-time high, bears want the breakout to be weak and fail quickly, forming a failed final flag.

- The market has traded sideways in a tight range for the past three months.

- Four consecutive dojis signal temporary balance between bulls and bears.

- Traders are watching whether this is a distribution phase or a bull flag setting up another leg higher in the months ahead.

- For now, traders will watch for a breakout in either direction and, more importantly, the strength of follow-through.

- Until then, the market may continue oscillating within the tight range in the near term.

Millennial Minute

It’s embarrassing to admit, but even I have fell victim to a scam or two in my time. Luckily, I’ve been able to catch it right away and deal with it, but it can leave you feeling so stressed and vulnerable!

Fraudsters perpetrate these crimes in a variety of ways, but many of the top scams have one thing in common: criminals are pretending to be someone they’re not.

Planning Article

Tax Tips for Investors

Knowing how the tax rules affect your investments is essential to maximizing your after-tax returns. Further, keeping up to date on changes to the tax rules may open up new opportunities, or could affect how your financial affairs should be structured.

The 2026 edition of Tax Tips for Investors provides ideas that you may incorporate into your wealth management strategy. As always, we recommend that you consult an independent tax professional to determine whether any of these tips are appropriate for your situation and to ensure the proper implementation of any tax strategies.